By Rudy Barnes, Jr.,

America has two separate economies: A booming stock market for the rich, and the wreckage of a pandemic economy for the rest. The Federal Reserve orchestrated a booming stock market that has increased disparities in wealth between the rich and the rest, and those disparities reflect a diminished middle class that threatens the stability of America’s democracy.

The Fed began propping up the mega-corporations of Wall Street following the recession of 2008 with low interest rates and subsidies euphemistically known as quantitative easing, but those generous benefits never reached Main Street. The stock market made a quick recovery, but the Fed policies favoring the rich over the rest continued to further disparities in wealth.

When the stock market crashed in March 2020 the Fed responded with $Trillions more in subsidies to mega-corporations and even lower interest rates, and Congress borrowed $Trillions to compensate the jobless. That produced an unprecedented recovery on Wall Street in just six months and a boom in the housing market that benefited the rich, but they did little for the rest.

Keynesian economists support modern monetary theory (MMT) that promotes more aggressive Fed monetary policies to benefit mega-corporations and the rich. They advocate more government spending and grants to stimulate consumer spending, and argue that creating more money and increasing the national debt do not threaten the economy.

Those Keynesian views conflict with traditional economic theory that creating more dollars reduces the value of existing dollars and that a national debt must one day be paid. America’s policy makers need to reconcile those conflicting monetary and economic theories and then find a solution to the increasing economic disparities between the rich and the rest.

The dominant issue over the next four years will be a post-pandemic economy. An astronomical national debt of $26.5 Trillion and increasing Federal Reserve purchases of bonds and corporate debt of over $4.5 Trillion threaten to crash the economy. Can America control its national debt and limit new money created by the Fed to stimulate the economy?

Ironically, Donald Trump used similar strategies of borrowing excessive amounts that he never intended to repay to create his own wealth--or the appearance of it. Bankruptcy is the remedy to end such financial fiascoes, but Trump used bankruptcy to intimidate his creditors to his advantage. MMT claims the U.S.can print its own money to avoid bankruptcy--but can it?

Before Trump reshaped the Republican Party and an economy that serves the rich and ignores the rest, the GOP supported responsible economic policies--even a balanced budget. That’s wishful thinking today. The future of America’s democracy depends on eliminating vast disparities in personal wealth, controlling its national debt and preserving the value of the dollar.

Notes:

Catherine Rampell has noted, “The U.S. has two economies. How much longer will the losing side stand for that? There’s the segment of the economy where retirement accounts are flush. Stock markets recently hit record highs, after all, thanks to loose monetary policy. Then there’s the large segment of the economy that owns no stocks, has little to nothing saved for retirement and isn’t sharing in this wealth creation. President Trump claims to have already vanquished the nation’s economic challenges — presumably because he’s looking at the economy as experienced by Mar-a-Lago members, and also because he hasn’t bothered to learn how little his own executive actions actually do. ...He proclaimed that any workers harmed by his boycott could easily “get another good jobs” because (thanks to his leadership) the labor market is already great again. Meanwhile, overall unemployment remains higher than it ever was during the Great Recession. New jobless claims are ticking up. Layoffs once hopefully considered “temporary” are being officially recategorized as “permanent.”

In the last presidential election, Trump rode to victory on a narrative that fat-cat Washington elites had ignored the struggles of the common man. Now Trump’s beloved working class has increasingly become an involuntarily non-working class, and Trump doesn’t bat an eye. To the extent he occasionally remembers their hardship, his administration’s chief strategy for helping them involves more tax cuts for the rich. “You want to help the blue-collars, cut the corporate tax rate. And I would put the capital gains rate in that category,” National Economic Council Director Larry Kudlow said last week. For context, the top 1 percent of households received three-quarters of all long-term capital gains last year. It’s truly a phenomenal feat of propaganda that the public still rates Trump as better on the economy than his presidential opponent, Joe Biden, despite the economic collapse the incumbent has presided over. Trump clearly believes it. Maybe Americans in the “good” economy do, too. At some point, though, the Americans left behind may start to notice, and resent, the victory party happening without them.” See https://www.washingtonpost.com/opinions/2020/08/20/us-has-two-economies-how-much-longer-will-losing-side-stand-that/?utm_campaign=wp_todays_headlines&utm_medium=email&utm_source=newsletter&wpisrc=nl_headlines.

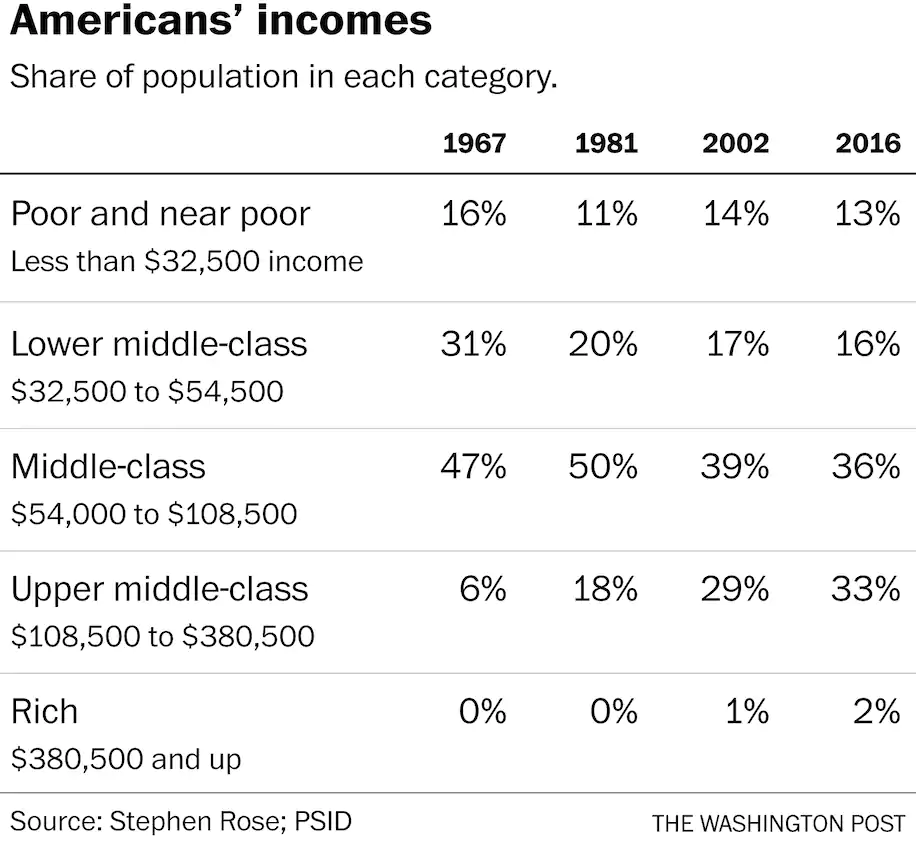

Robert Samuelson has cited a study by Stephen Rose that indicates a significant rise of the upper-middle class while there has been a drop in the lower middle-class and middle-class. It reflects increasing disparities in the wealth of Americans, and a diminishing middle class portends political volatility.

“The Federal Reserve is undergoing an overhaul. Conceived to keep inflation in check and oversee the country's money supply, the central bank is now essentially directing the economy and moving away from worries about rising prices.” Scott Minerd, CIO of Guggenheim Partners, has asserted that ‘Free market enterprise no longer exists.’ The Fed ...has taken control of the market. ‘The definition of market prices is whatever the Fed says it will be,’ says Minerd.’” Since the Fed's unprecedented intervention into credit markets in late March, it has become a general understanding stated openly by economists and asset managers, including those at high-profile investment firms like Deutsche Bank and Bank of America. But not all of the Fed's new programs have worked as planned. After significant delays, its $600 billion Main Street Lending Program has provided less than one-tenth of 1% of its allotted funding to needy small businesses even as the Paycheck Protection program has whiffed and business closures have spiked. Compare that to the trillions it has used on QE and the billions it has purchased in debt from some of the country's largest companies using a backstop of taxpayer money and it's no wonder politicians and economists have called the Main Street program a "failure" and an "unmitigated disaster." See https://www.axios.com/federal-reserve-policy-inflation-7b569f0c-a27d-45d1-a075-2b276f252efc.html.

See also, The Federal Reserve’s new Inflation target redefines the meaning of inflation at https://www.forbes.com/sites/johntamny/2020/08/09/the-federal-reserves-new-inflation-target-is-insulting-and-backwards/#614be0ea3709.

Wolf Richter has observed: “We now have the Pandemic Economy with the Incredibly Spiking US Gross National Debt, which spiked incredibly by $4.45 trillion over the past 12 months to $26.5 trillion. Whoosh go the trillions, flying by. These are all Treasury Securities, and someone had to buy them, but who? With the Treasury Department’s Treasury International Capital (TIC) data through June 30, and with other data released by the Federal Reserve, we can piece together who bought those $4.45 trillion in Treasury Securities over the past 12 months. Foreign central banks, governments, companies, commercial banks, bond funds, other funds, and individuals, all combined added $90 billion to their holdings in June. Over the 12-month period through June, they added $413 billion. They now hold a total of $7.04 trillion, a huge record pile. But given the incredibly spiking US Treasury debt ($26.45 trillion on June 30), their share of this debt plunged to just 26.6%, the lowest since 2008. Japan and China, the two largest foreign creditors of the US, combined held 8.8% of the US debt, the lowest share going back many years. Back at the end of 2015, their combined holdings were still 12.8% of the total US debt. Japan maintained its holdings in June for the third month in a row at $1.26 trillion, but over the 12-month period increased its holdings by $138 billion. China cut its holdings in June by $9 billion, to $1.07 trillion, and over the 12-month period by $38 billion. Despite the mega-trade deficits that the US has with Mexico and Germany, their holdings of US Treasury securities are relatively small: Germany held $80 billion and Mexico $47 billion.

The Social Security Trust Fund, pension funds for federal civilian employees, pension funds for the US military, and other government funds added $50 billion in June and $112 billion over the 12-month period to their holdings, which reached $5.95 trillion, or about 22.5% of total US debt. These Treasury securities, often called “debt held internally,” represent assets that belong to the beneficiaries of those funds. They’re a true debt of the US, and they don’t go away – just because American beneficiaries are indirectly the holders of these assets. In June, the Fed added just $95 billion to its pile of Treasuries, having already cut back its purchases, after having added $1.6 trillion from March 11 through the end of May, bringing its total holdings at the end of June to $4.2 trillion. It holds about 15.9% of the US debt.

Over the 12-month period, the Fed added $2.1 trillion in Treasuries to its holdings, about doubling its pile over the period (weekly chart through August 12): Just over the month of June, US commercial banks added $121 billion in Treasury securities, to a total of $1.07 trillion. This brought the 12-month increase to $220 billion. They hold about 4.0% of the total US debt. That’s everything that is not included in the above. By the end of June, over the course of the tumultuous second quarter, these US entities added $1.6 trillion, after having been big sellers of Treasuries in prior quarters. This brought their total holdings to a mega-record of $8.13 trillion – about 31% of the total US debt. For charts on the above, see

Bloomberg (8/14/2020) reports: “Like it or not, Modern MonetaryTheory (MMT) Experiment is Underway.

Robert Hormats says the pandemic has forced the ‘involuntary utilization’ of MMT. ‘Well, now we have a particularly unusual set of circumstances whereby we're in the midst of forced, or involuntary, utilization of modern monetary theory…This is not unheard of. ...It was done during World War II, where the Fed guaranteed the Treasury that it would buy Treasury bonds at a very low rate to keep interest rates low to keep the debt servicing costs of the government low. So theoretically, this can last a very long time as long as the Treasury is making these big bond issues a regular occurrence as it appears. And the Fed’s Jay Powell has said he is going to, in effect, continue to keep rates low. But he said also: ‘The Fed can't do it all and the Fed cannot do this indefinitely.' But what is indefinite? How long can this occur? What are the end results of this, at some point, if trees don't grow to the sky? What could disrupt the markets and what could cause either the Treasury to run into trouble with its issues, or the Fed to feel uncomfortable underwriting those issues for the indefinite future? We don't know that. This is all terra incognita.’” See https://www.bloomberg.com/news/articles/2020-08-14/like-it-or-not-a-modern-monetary-theory-experiment-is-underway. See also, article on MMT below.

Gareth Huttchens provides an overview of Modern Monetary Theory by listing six claims made by MMT proponents: “First, they say we've been thinking about budget deficits incorrectly. They say that budget deficits are not always bad. In fact, deficits are often necessary and beneficial. A budget deficit is merely evidence of extra government spending, and government spending boosts the wealth of private sector businesses and households. Investments that will enhance productivity through better health, greater knowledge and skills, improved transport and the like are worth funding, even if it results in a budget deficit. Second, MMT economists say we've been thinking about government spending incorrectly. They say the argument that national governments must tax or borrow before they can spend is wrong. MMT argues it's the other way around--national governments have to spend money into the economy before they can tax or borrow. Government spending actually precedes taxation. Third, they say taxes are necessary, but not for the reasons you may think. Government taxes can be used to keep inflation under control, to control our behavior (via fees and levies and rates), and to get us to produce things the government needs. They say governments use taxes to create demand for their own currency--that is, if a citizen has to pay tax then they're going to have to work to earn the currency to pay the tax in that currency. Essentially, governments use taxes to put everyone to work. Fourth, MMT economists say countries that issue their own fiat currency can afford to buy anything that's available for sale in their own currency, and they can never go bankrupt in their own currency. "Fiat" money is government-issued currency that isn't backed by any commodity, such as gold. Fifth, MMT economists say "full employment" is not only possible, it's a moral imperative. Anyone who wants a job should have one. They say we must prioritise genuine full employment and governments should spend whatever is necessary to achieve it — no matter the debt or deficit. Sixth, MMT economists say the national government should run a permanent "Job Guarantee" (JG) program to provide a job to everyone who wants one. It could be linked to other economic and social programs, such as a ‘Green New Deal’ advocated by MMT proponents linked to US Democratic senator Bernie Sanders to create jobs with zero-emissions technologies.”

Among the many critics of MMT is Stephen Grenville, a former deputy governor of the RBA. He argues, “There's no free lunch. The chief vulnerability of the MMT narrative, and where MMT economists "are a little vague, even slippery," is the MMT assumption that budget deficits can be funded without adding to official debt. "The government might get the cash to spend in its deficit by giving the central bank a bond in return for the cash." But the bond is just a government debt which it owes itself, so in the view of many MMT supporters, the bond could be deleted from the central bank balance sheet by offsetting book entries in the accounts of the government and the central bank. "This seems to be 'free money'," he said. "It's hardly surprising that this is an attractive narrative [but] this is clearly wrong."

Another concern about MMT is in bond markets, where “traders may decide that your currency will become nearly worthless if your leaders start printing money and expanding the budget deficit. Financial market participants may take a lot of convincing.”

see https://www.abc.net.au/news/2020-07-17/what-is-modern-monetary-theory/12455806.

No comments:

Post a Comment